A number stopped me cold last year. Sitting at my desk on a Tuesday morning, coffee going lukewarm, reading a Government Accountability Office report Maggie had flagged for me. (She reads the news digest while I read the Journal. We divide and conquer.) The number: roughly one-third of veterans over 65 who qualify for VA benefits related to long-term care have never applied. Not denied. Never applied. They don't know the benefits exist, or they assume they don't qualify, or they tried once, got buried in paperwork, and gave up.

Not a policy failure. A communication failure. And it's personal for me.

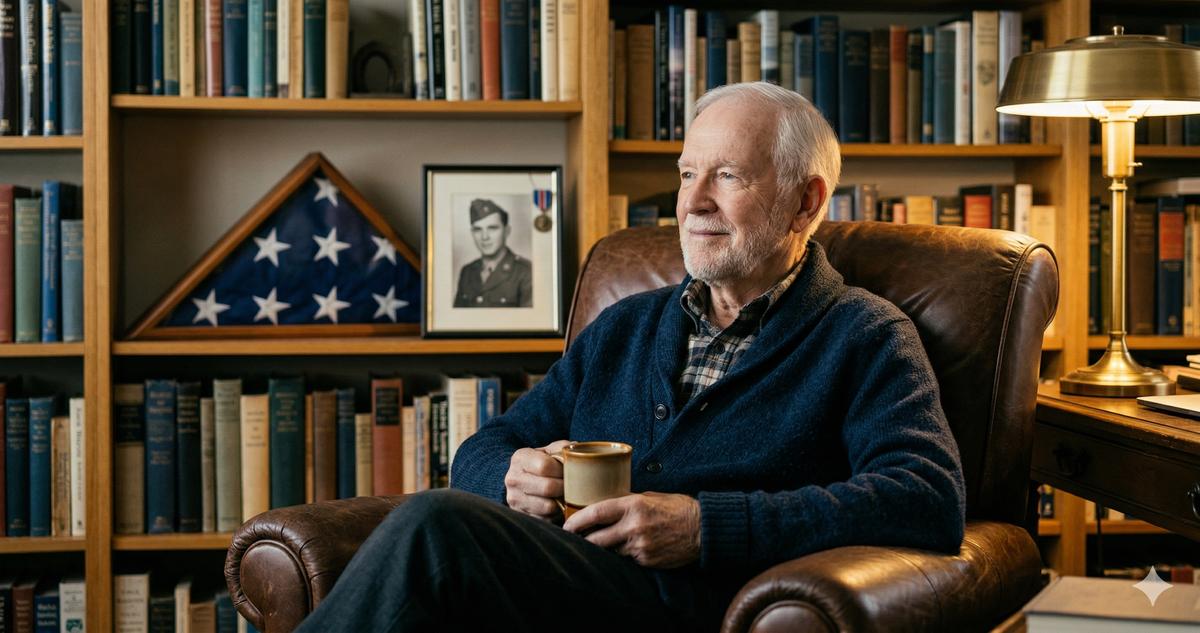

My father Arthur spent 40 years at Pratt & Whitney in East Hartford, machining turbine blades for jet engines. What I rarely mention in these articles: before Pratt & Whitney, Arthur served two years in the Army, stationed at Fort Riley in Kansas from 1956 to 1958. He never saw combat. He drove supply trucks on a base in the middle of Kansas, came home, married my mother Ruth, and went to work in the machine shop. He never thought of himself as a veteran in the way the word gets used on television. He was just a guy who did his two years.

When Arthur's health declined in his late seventies, Months went to figuring out Medicaid, assisted living costs, Medicare supplement plans. It never occurred to me to look into VA benefits. A financial planner with 30 years of experience, and I didn't check. Arthur qualified for Aid and Attendance. He qualified for VA health care enrollment. He qualified for the Connecticut State Veterans Home in Rocky Hill, which would have cost a fraction of what we paid at the private facility in Hartford. By the time a colleague mentioned it to me over coffee, Arthur was gone.

The missed conversation haunts me more than I'd like to admit. So here's the guide I should have had. Every dollar amount, every form number, every phone number. If your parent served, or if your parent's spouse served, keep reading.

Who Qualifies: The Eligibility Question Most Families Get Wrong

The single biggest misconception I encounter is this: "My father wasn't in combat, so he doesn't qualify for VA benefits." Wrong. Not even close.

VA benefits for senior care are not limited to combat veterans. They're not limited to veterans with service-connected disabilities. The eligibility requirements for the programs most relevant to aging veterans are far broader than most families realize.

For VA health care enrollment, the basic requirements are:

- Served on active duty (not just reserves, though some reservists qualify)

- Received an honorable or general discharge

- Meet minimum service length (generally 24 continuous months or the full period called to active duty, though veterans who served before September 7, 1980, have different rules)

No combat requirement. No injury requirement. No income requirement for enrollment itself, though income affects copays and priority group placement.

For the pension-based benefits covering senior care, including Aid and Attendance, the requirements add a wartime service element. Your parent must have served at least 90 days of active duty, with at least one day during a wartime period. The wartime periods covering most living veterans:

- Korean War: June 27, 1950 to January 31, 1955

- Vietnam Era: February 28, 1961 to May 7, 1975 (August 5, 1964, for non-Vietnam theater)

- Gulf War: August 2, 1990 to present (yes, still ongoing for VA purposes)

Arthur served from 1956 to 1958. Between the Korean and Vietnam periods. He missed the wartime window by 11 months. Eleven months! If he'd enlisted a year earlier, he'd have qualified for the pension. The dates are absolute. No exceptions, no appeals on the dates themselves.

But here's what many families miss. If your parent served during a wartime period, even if they never left the United States, even if they spent their entire service filing paperwork at a desk in Virginia, they meet the wartime requirement. A supply clerk at Fort Bragg during Vietnam qualifies the same as a combat infantryman for pension purposes.

For surviving spouses, the veteran doesn't need to be alive. If your mother's late husband served during a wartime period and met the other requirements, she may qualify for Dependency and Indemnity Compensation or the Survivors Pension with Aid and Attendance. Hundreds of thousands of widows and widowers qualify and have never filed.

Aid and Attendance: The Benefit Nobody Talks About

The program should have been on my radar for Arthur. Aid and Attendance is an enhanced VA pension for veterans (and surviving spouses) who need help with daily activities or are housebound.

The 2026 maximum monthly rates:

- Veteran without dependents: $2,050/month ($24,600/year)

- Veteran with one dependent (usually a spouse): $2,431/month ($29,172/year)

- Surviving spouse: $1,318/month ($15,816/year)

- Housebound veteran without dependents: $1,510/month

- Housebound veteran with one dependent: $1,881/month

Those numbers are tax-free. Every dollar. No federal income tax, no state income tax. A married veteran receiving $2,431 per month in Aid and Attendance is getting the equivalent of roughly $3,000 in pre-tax income, depending on their bracket.

To qualify, your parent must meet all of these:

- Wartime service (90 days active, one day during a wartime period, honorable discharge)

- Financial need (limited income and net worth; more on this below)

- Medical need (needs regular aid of another person for daily activities, is bedridden, is a patient in a nursing home, or has corrected visual acuity of 5/200 or less in both eyes)

The financial limits for 2026:

Net worth limit: $155,356 (adjusted annually for inflation). This includes all countable assets plus annual income. The VA uses a "bright line" test introduced in 2018. If your parent's total net worth (assets plus projected annual income) exceeds $155,356, they don't qualify. Below it, they do.

But wait. The family home doesn't count. One vehicle doesn't count. Personal property doesn't count. The net worth calculation covers financial assets: bank accounts, investments, IRAs, stocks, bonds. If your parent owns a $300,000 house, drives a paid-off car, and has $80,000 in savings with $24,000 in annual income, their countable net worth is approximately $104,000. Under the limit.

The three-year look-back is the trap. In 2018, the VA implemented a three-year look-back period for asset transfers. Any gifts or transfers made to reduce net worth below the $155,356 threshold during the 36 months before the application will trigger a penalty period. Sound familiar? It's similar to Medicaid's five-year look-back, but shorter.

George was 84, a retired electrician from Bridgeport who'd served 14 months in the Army during the Vietnam era. Never went overseas. Spent his service at Fort Leonard Wood in Missouri, training other soldiers on electrical systems. His daughter brought him to a workshop I did at the Westport Senior Center on a rainy Saturday in March 2024. George had Parkinson's. His wife Helen, 81, was providing all his care. Their savings were $112,000, his pension and Social Security totaled $3,200 per month, and Helen's Social Security was $1,380. Combined annual income: $54,960. Combined net worth including income: $166,960. Just over the limit.

We looked at the numbers together. George had $14,000 in unreimbursed medical expenses from the past year: home health aides, a wheelchair ramp, incontinence supplies, prescription copays. The VA allows you to deduct unreimbursed medical expenses from income for pension calculations. The deduction dropped his countable income, and his adjusted net worth fell below the threshold.

George was approved four months later. $2,431 per month. Tax-free. Helen cried in my office. Not the first time. Every time it hits the same.

VA Health Care Enrollment: More Than Most Families Expect

Separate from the pension, the VA operates one of the largest health care systems in the country: 1,321 facilities, including 171 VA Medical Centers and over 1,100 outpatient clinics. Enrollment is based on priority groups, and most veterans over 65 qualify.

The eight priority groups determine copays and access:

- Group 1: Veterans with 50% or higher service-connected disability. No copays for anything.

- Groups 2-3: Veterans with 30-40% disability, former POWs, Purple Heart recipients, catastrophically disabled. Minimal or no copays.

- Group 4: Housebound veterans or those receiving Aid and Attendance.

- Group 5: Veterans with income below the VA's geographic threshold and those receiving VA pension. No copays.

- Groups 6-7: Various categories including Agent Orange exposure, Gulf War illness, and moderate-income veterans. Some copays.

- Group 8: Higher-income veterans with no service-connected conditions. Copays apply, but still often less than private insurance.

What VA health care covers, and what surprises people:

- Primary care, specialty care, mental health, and prescription drugs

- Dental care (limited, but available for some priority groups)

- Vision care including eyeglasses

- Hearing aids at no cost for most enrolled veterans

- Home health services

- Adult day health care

- Respite care for family caregivers (up to 30 days per year)

- Geriatric evaluation and management

- Hospice and palliative care

The prescription drug benefit alone can save thousands. VA pharmacy copays in 2026 are $5 for a 30-day supply of Tier 1 medications and $11 for Tier 2. Compare it to Medicare Part D, where the average copay runs $10 to $47 depending on the tier and formulary. A veteran taking four medications could save $1,200 to $2,400 annually on prescriptions alone.

To enroll, your parent needs one form: VA Form 10-10EZ, Application for Health Benefits. Available at va.gov/health-care/apply-for-health-care-benefits/ or by calling 1-877-222-8387. Processing takes 7 to 10 business days for most applications. Bring the DD-214 (discharge papers). If your parent can't find their DD-214, request a replacement from the National Personnel Records Center at archives.gov/veterans or call 314-801-0800. Replacement requests take 10 to 90 days depending on the era of service.

One thing I wish more families knew: VA health care and Medicare work together. Your parent can be enrolled in both. Many veterans use the VA for primary care and prescriptions (cheaper copays) and Medicare for specialists or situations where the nearest VA facility is hours away. They're not competing systems. Use both.

Geriatrics and Extended Care: The VA Programs Families Don't Know About

The VA's Geriatrics and Extended Care (GEC) division runs programs specifically designed for aging veterans. These are separate from standard VA health care and many have no copay at all.

Home Based Primary Care (HBPC): A VA team, typically a doctor, nurse, social worker, dietitian, and pharmacist, comes to your parent's home. Not occasionally. Regularly. This program serves veterans who have complex, chronic health conditions and difficulty getting to a VA facility. I've seen it described as "the VA version of a house call," which undersells it. HBPC teams manage medications, coordinate specialist referrals, provide caregiver training, and monitor conditions otherwise requiring repeated ER visits.

Community Nursing Home Program: The VA contracts with private nursing homes near the veteran's family when VA facilities aren't available or appropriate. The VA pays directly. Eligibility varies by priority group, but veterans with 70% or higher service-connected disability, or those needing nursing home care for a service-connected condition, can receive VA-paid nursing home care indefinitely.

State Veterans Homes: Every state operates veterans homes, partially funded by the VA. These are nursing homes, assisted living facilities, and domiciliary care facilities reserved for veterans. There are 158 state veterans homes across the country. The daily rates are typically 30% to 50% lower than comparable private facilities because the VA pays a per diem directly to the state. Connecticut operates two: the Connecticut State Veterans Home in Rocky Hill and a residential facility in West Haven. Arthur could have been at Rocky Hill. Twenty-three minutes from my mother Ruth's assisted living in Hartford. I could have visited them both on Sundays.

I need to move on from this one.

Adult Day Health Care: VA-run or VA-contracted day programs providing health services, socialization, and supervision during daytime hours. Available at VA Medical Centers and through community partnerships. No copay for most enrolled veterans.

Veteran-Directed Care: This one is remarkable and almost nobody has heard of it. The veteran receives a budget from the VA and hires their own caregivers, including family members. Similar in concept to California's IHSS program but available nationally through participating VA Medical Centers. The veteran, with help from an agency, decides how to spend the care budget: hiring aides, purchasing equipment, paying for home modifications. Roughly 230 VA facilities offer this program as of 2026.

Medical Foster Home: For veterans who can't live independently but don't need a nursing home, the VA's Medical Foster Home program places veterans in private homes with trained caregivers. A VA team provides regular oversight. The veteran typically pays a negotiated rate to the foster home caregiver, often $1,500 to $3,000 per month, far less than assisted living. Aid and Attendance can cover much or all of this cost.

The VA Caregiver Support Program

If your parent is a veteran and you're providing their care, or if you're the veteran yourself and your spouse or child is your caregiver, this section matters.

The VA operates two caregiver programs:

Program of General Caregiver Support Services: Available to caregivers of veterans enrolled in VA health care from any service era. Provides education, training, a support line (1-855-260-3274), peer mentorship, respite care referrals, and access to the Caregiver Support Coordinator at your parent's VA Medical Center. No formal application. Call the support line and ask for a referral.

Program of Comprehensive Assistance for Family Caregivers (PCAFC): The bigger program. Expanded to all eras in October 2020, PCAFC provides a monthly stipend to the primary caregiver based on the level of care needed. The stipend is tied to the GS pay scale for the veteran's geographic area and ranges from roughly $800 to over $3,000 per month depending on the care tier. The caregiver also gets CHAMPVA health insurance (if otherwise uninsured), mental health counseling, and 30 days of respite care per year.

Eligibility for PCAFC requires the veteran to have a serious injury (physical or mental, including traumatic brain injury and PTSD) incurred or aggravated in the line of duty. The veteran must need at least six months of continuous personal care services. A VA clinical team evaluates the application.

The stipend is significant. A caregiver providing full-time care to a Tier 3 veteran in the New York City or San Francisco area can receive over $3,200 per month. In lower-cost areas, the range is typically $1,900 to $2,600. Tax-free.

Herbert was 79, a Marine Corps veteran who'd served in Vietnam from 1968 to 1970. Came home with hearing damage and knees wrecked by 14 months of patrol. His wife Constance, 76, had been managing his medications, driving him to appointments, helping him in and out of the shower, and handling the household on her own since his mobility declined sharply after a fall in 2023. She was exhausted. At a caregiver support group at the West Haven VA, a social worker asked her if she'd applied for PCAFC. She hadn't. She didn't know it existed.

Constance was approved as Herbert's primary caregiver. Tier 2 stipend: $2,180 per month. She also enrolled in CHAMPVA, saving them $4,800 per year in her Medicare supplement premiums. And she got 30 days of respite care, which meant someone came to the house once a month so she could spend the day with her sister in Milford without worrying.

Constance told me the stipend was nice, but the respite days were what kept her going. "I didn't know I was drowning until someone threw me a rope," she said. Her words have stayed with me.

CHAMPVA: Health Coverage for Surviving Spouses

If your parent is the surviving spouse of a veteran who died from a service-connected condition, or the spouse of a veteran with a permanent and total service-connected disability, CHAMPVA provides health coverage.

CHAMPVA (Civilian Health and Medical Program of the Department of Veterans Affairs) works like health insurance. It covers:

- Doctor visits and hospital stays

- Outpatient care and surgery

- Mental health services

- Prescription drugs

- Durable medical equipment

- Skilled nursing facility care (limited)

- Hospice care

- Home health services

The costs are low. Annual deductible: $50 per person, $100 per family. Cost share: 25% of the allowable amount after the deductible. Catastrophic cap: $3,000 per calendar year per family. Beyond the cap, CHAMPVA pays 100%.

CHAMPVA and Medicare can work together. If your parent has both Medicare and CHAMPVA, Medicare pays first, and CHAMPVA covers most of the remaining costs. The combination often eliminates out-of-pocket expenses entirely, making it more cost-effective than many Medigap supplement plans.

Application form: VA Form 10-10d. Submit to: VHA Office of Community Care, CHAMPVA, P.O. Box 469028, Denver, CO 80246-9028. Or fax to (303) 331-7809. Processing time: 6 to 8 weeks.

How to Apply for Aid and Attendance: The Paperwork, Step by Step

I'm going to walk through this like I'm sitting across from you at my desk with a legal pad. Because it's essentially what I do with families in my office, and the process is the same whether you're in Westport or Wichita.

Step 1: Find the DD-214.

The DD-214, Certificate of Release or Discharge from Active Duty, is the foundational document. Without it, the VA can't verify service. Check your parent's files, their safe deposit box, and the shoebox in the closet. If it's lost, request a copy from the National Personnel Records Center: archives.gov/veterans or 314-801-0800. You can also submit SF-180 (Request Pertaining to Military Records) by mail. Be patient. These requests take anywhere from two weeks to three months.

Step 2: Get a medical evaluation.

Your parent's doctor needs to complete a medical statement documenting the need for aid and attendance. The VA's form is VA Form 21-2680, Examination for Housebound Status or Permanent Need for Regular Aid and Attendance. The doctor fills out the clinical sections describing what your parent can and can't do: bathing, dressing, feeding, toileting, ambulating, cognitive functioning. The more specific the doctor is, the stronger the application. "Patient requires assistance" is weak. "Patient cannot stand unassisted, requires physical support to transfer from bed to wheelchair, cannot button clothing due to severe arthritis in both hands, and is unable to safely prepare meals due to cognitive impairment" is strong.

If your parent is in a nursing home, the facility's medical director can complete the form.

Step 3: Gather financial documents.

The VA needs a full picture of your parent's finances:

- Social Security benefit verification letter

- Pension statements

- Bank statements (checking, savings, investment accounts)

- Documentation of unreimbursed medical expenses (this is critical for reducing countable income)

- Real estate records (to confirm the home is the primary residence)

- Any annuity or life insurance documentation

Step 4: Complete VA Form 21-534EZ (for surviving spouses) or VA Form 21-527EZ (for veterans).

The 21-527EZ is the Application for Veterans Pension. Aid and Attendance is an enhancement of the pension, not a separate program. You apply for the pension and check the box requesting Aid and Attendance. The form asks for service dates, discharge status, income, assets, medical conditions, and marital status.

The 21-534EZ is the Application for Dependency and Indemnity Compensation, Death Pension, and Accrued Benefits by a Surviving Spouse or Child. The surviving spouse version.

Step 5: Submit the application.

Three ways:

- Online: va.gov (create or log into a VA.gov account)

- By mail: Department of Veterans Affairs, Pension Intake Center, P.O. Box 5365, Janesville, WI 53547-5365

- In person: At your regional VA office or through a Veterans Service Organization (VSO)

Actually, I want to correct myself. The single best way to file is through a Veterans Service Organization. The American Legion, VFW, DAV (Disabled American Veterans), and state veterans service offices all have accredited claims agents who file these applications every day. They know the forms, they know the common mistakes, and their help is free. Completely free. I cannot stress this enough. The application process has a learning curve. A VSO representative has already climbed it.

Find accredited representatives at va.gov/vso/ or call your state's Department of Veterans Affairs.

Step 6: Wait. Then follow up.

Average processing time for pension claims with Aid and Attendance: 90 to 180 days. Some go faster. Some go much slower. If you haven't heard anything in 90 days, call the VA at 1-800-827-1000 and ask for a status update on the claim. The VA assigns a case number when you file. Keep it.

While you wait, keep paying for care. Aid and Attendance, if approved, can be backdated to the date of the original application. If your parent applied on March 1 and gets approved on September 15, they receive a lump-sum payment covering March through September. For a married veteran: $2,431 times six months, or $14,586. Families sometimes forget this. Don't forget this.

Common Denial Reasons and How to Appeal

Denials happen. About 25% of initial pension claims are denied, and the reasons are almost always fixable.

The most common denial reasons:

- Net worth above $155,356 (assets weren't properly documented or medical expense deductions weren't included)

- Insufficient medical evidence (the doctor's statement on VA Form 21-2680 was too vague)

- Service dates don't meet wartime requirements

- Discharge status other than honorable (a "general under honorable conditions" discharge usually qualifies, but a "bad conduct" discharge typically doesn't)

- Missing DD-214 or inability to verify service

Your appeal options:

Since the Appeals Modernization Act of 2019, veterans have three pathways:

- Supplemental Claim: Submit new evidence missing from the original application. The most common path and often the fastest. If the denial was for insufficient medical evidence, get a more detailed doctor's statement and refile. Form: VA Form 20-0995.

- Higher-Level Review: A senior VA reviewer takes a fresh look at the same evidence. No new evidence allowed. Best used when you believe the original decision misapplied the rules. Form: VA Form 20-0996. Average processing: 125 days.

- Board of Veterans' Appeals: A Veterans Law Judge reviews the case. You can submit new evidence, request a hearing, or both. The longest route (12 to 24 months) but sometimes necessary. Form: VA Form 10182.

Free help with appeals:

- Veterans Service Organizations (American Legion, VFW, DAV): free accredited representatives

- State veterans service offices: free claims assistance

- Legal aid through the National Veterans Legal Services Program: nvlsp.org

- VA's toll-free hotline: 1-800-827-1000

Kenneth was 88, a Navy veteran who served on a destroyer escort during the Korean War. His initial Aid and Attendance claim was denied because the medical evidence was insufficient. His primary care doctor had written, "Mr. [redacted] requires some assistance with daily activities." Some assistance. Might as well tell a mortgage lender your client has "some income." Kenneth's daughter contacted the DAV, and an accredited representative helped her get a detailed occupational therapy evaluation. The OT documented Kenneth couldn't stand from a seated position without a grab bar, needed hands-on assistance to shower, could not manage his nine medications without supervision, and had fallen three times in the previous four months. The supplemental claim was approved in 47 days.

The medical evidence is the application. Treat it accordingly.

Every Number, Website, and Form You Need

I keep a printed version of this in my client files. You should keep one too.

VA Contact Numbers:

- VA Benefits Hotline: 1-800-827-1000 (Monday-Friday, 8 AM to 9 PM ET)

- VA Health Care Enrollment: 1-877-222-8387

- Caregiver Support Line: 1-855-260-3274

- Veterans Crisis Line: 988, then press 1 (or text 838255)

- CHAMPVA: 1-800-733-8387

- National Personnel Records Center (DD-214 requests): 314-801-0800

Key Websites:

- VA.gov: va.gov (central hub for all benefits)

- VA Health Care Application: va.gov/health-care/apply-for-health-care-benefits/

- VA Pension Information: va.gov/pension/

- Find VA Locations: va.gov/find-locations/

- Find a VSO: va.gov/vso/

- DD-214 Replacement: archives.gov/veterans

- CHAMPVA: va.gov/health-care/family-caregiver-benefits/champva/

- Benefits Screening: benefitscheckup.org

- Eldercare Locator: 1-800-677-1116

Key Forms:

- VA Form 10-10EZ: Health Care Application

- VA Form 21-527EZ: Application for Veterans Pension (includes Aid and Attendance)

- VA Form 21-534EZ: Application for DIC, Death Pension, and Accrued Benefits (surviving spouses)

- VA Form 21-2680: Examination for Housebound Status or Permanent Need for Regular Aid and Attendance

- SF-180: Request Pertaining to Military Records (DD-214 replacement)

- VA Form 10-10d: CHAMPVA Application

- VA Form 20-0995: Supplemental Claim

- VA Form 20-0996: Higher-Level Review

- VA Form 10182: Board of Veterans' Appeals

Veterans Service Organizations (Free Help):

- American Legion: legion.org, 1-800-433-3318

- VFW (Veterans of Foreign Wars): vfw.org, 1-800-VFW-1899

- DAV (Disabled American Veterans): dav.org, 1-877-426-2838

- Vietnam Veterans of America: vva.org, 1-800-882-1316

- National Veterans Legal Services Program: nvlsp.org

State Veterans Homes:

- NASVH (National Association of State Veterans Homes): nasvh.org

- 158 state veterans homes nationwide; find yours through va.gov/find-locations/ or your state's Department of Veterans Affairs

The Scams Targeting Veterans

It would be irresponsible not to mention this. The benefits described in this guide are real, administered by the VA, and free to apply for. But an entire industry of predatory companies charges veterans $2,000 to $10,000 to file claims the VA processes at no cost!

Red flags:

- Any company that charges upfront fees to file VA pension claims. Accredited VSOs do this for free

- "Pension poachers" who contact veterans or widows unsolicited, often after obtaining information from public records or funeral notices

- Financial advisors (and I use the term loosely) who restructure a veteran's assets to qualify for Aid and Attendance, then charge a percentage of the benefit. Asset restructuring can trigger the three-year look-back penalty and the financial advice itself violates VA regulations if the advisor isn't accredited

- Companies selling annuities to veterans as a way to "spend down" assets for pension eligibility. The VA specifically watches for these transactions and will impose penalty periods

A retired postal worker from Norwalk, 82, told me at a workshop: a company had charged his wife $3,500 to fill out her Survivors Pension application after he mentioned his Army service at a senior center event. The company had done nothing the DAV wouldn't have done for free. His wife didn't know. She thought $3,500 was the cost of applying. It is not. It should never be.

If anyone asks you to pay to file a VA claim, walk away. Call 1-800-827-1000 or visit your local VFW or American Legion post. The person behind the counter has filed a hundred of these. They will help you for nothing because the organization exists to do exactly one thing: help veterans. Our guide on how to spot scams targeting seniors covers the broader patterns worth knowing.

What Arthur Would Have Wanted Me to Tell You

Arthur Wells wasn't a man who talked about his service. He kept his discharge papers in a manila envelope in the bottom drawer of his dresser, underneath his good shirts. The papers turned up three months after he died while cleaning out his room at the assisted living facility. The envelope was yellowed at the edges. I don't think he'd opened it in 40 years.

He would have been embarrassed by this article, honestly. He'd have said the benefits should go to the people who "really served," meaning the ones who saw combat, the ones who came home different. He carried his quiet modesty to the grave. And it cost him, and cost our family, benefits he'd earned.

Every veteran earned them. Desk clerks and infantry. Mechanics and medics. The ones who served two years in Kansas and the ones who served three tours overseas. The benefits exist because the country made a promise, and the promise doesn't come with an asterisk.

If your parent served, or if your parent's spouse served:

- Find the DD-214. Bottom drawer, safe deposit box, the envelope nobody's opened since 1972. If it's gone, call 314-801-0800 and request a replacement.

- Call 1-800-827-1000 tomorrow morning. Ask about VA health care enrollment and pension eligibility. Have the DD-214 and your parent's Social Security number ready.

- Contact a Veterans Service Organization. The American Legion, VFW, or DAV in your parent's county will assign an accredited representative. Free.

- If your parent needs daily help with bathing, dressing, or mobility, ask their doctor to fill out VA Form 21-2680 with specific, detailed language.

- If your parent is a surviving spouse wondering about available benefits, ask about Survivors Pension with Aid and Attendance and CHAMPVA.

Every Sunday, the drive to Hartford takes me to my mother Ruth. She's 89. She doesn't always know who I am, but she always asks if I've eaten. On the way home, I pass the Connecticut State Veterans Home in Rocky Hill. Thirty-one miles from Ruth's facility. Arthur should have been there. The room would have cost less. The care was rated excellent. And I would have visited them both every Sunday, same drive, same route, same true crime podcast, just one extra stop.

I can't go back. But you can go forward. The forms are on va.gov. The phone number is 1-800-827-1000. The people on the other end have answered this question a thousand times. Let them answer it for you.